Billions and Billions: Private Equity Investments in Collision Repair Surge

In the last five months, more than $9 billion in capital has been invested into the collision repair industry by private equity firms. The biggest chunk of this new capital was $4.6 billion in debt refinancing by Caliber Collision. Crash Champions also refinanced a significant piece of its debt and brought in an additional equity investment. Classic Collision, CollisionRight, VIVE Collision and Kaizen all found new sponsors. As the industry’s leading M&A advisor, we have thoughts and comments.

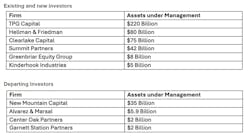

Caliber issued new debt to refinance existing debt and fund a significant dividend for the current shareholders. Crash Champions refinanced some short-term debt and raised some additional equity which it is deploying into more acquisitions. The original private equity sponsors of VIVE Collision, Garnett Station Partners, sold to a larger private equity firm, Greenbriar Equity Group, which has significant holdings in the automotive aftermarket sector.

Similarly, Center Oak Partners, the original private equity sponsor of CollisionRight, sold the company to Summit Partners, a much larger private equity firm.

And Kinderhook Industries, echoing a prior investment in the collision repair industry, became the lead investor in Kaizen Collision along with Kaizen’s existing investors. Kinderhook had previously invested in ProCare, supported its investment in Austin Motor Mile, and then sold out to Classic Collision.

Classic Collision, after less than five years with its primary sponsor, New Mountain Capital, announced a recapitalization with new sponsor TPG Capital, the private equity arm of the $220 billion AUM publicly traded global asset management firm TPG.

We estimate the total amount invested over the last five months exceeds $9 billion.

The Investors: A Rotation of Sponsors from Smaller to Larger

To put all of this in perspective, the private equity sponsors in the collision repair industry today - both those exiting sponsors and the incoming ones - collectively manage more than $400 billion in managed assets.

The private equity sponsors that have recently entered the industry or increased their positions have largely supplanted smaller private equity firms. The most recent transaction, TPG Capital’s acquisition of Classic Collision, introduced one of the world’s largest alternative investment funds to the industry.

Why Now?

At a time when interest rates are significantly higher than they were a year ago, why is all this new capital coming into the industry? It seems counterintuitive when interest rates are so high, that companies would accelerate their capital raising. What's going on?

Large private equity firms see an opportunity to accelerate their growth as the availability and cost of their capital vastly exceeds smaller players and independent shops. Another reason is that the increased revenues - driven by higher labor rates and calibration - have positively impacted EBITDA margins, making them more attractive to lenders and new investors. And there's also the ongoing attractiveness of arbitraging acquisitions. Buying strong single shops and small MSOs at five to seven times EBITDA while raising capital at valuations of 12 to 14 times allows this new capital to effectively leverage their superior capital into faster growth.

Early investors are more willing to take higher risks

Early private equity investors take more risks when they acquire platforms and then bolt on additional MSOs and single shops. They are supporting management teams that may not have proven themselves in operating at a much larger scale or buying and integrating multiple targets in a shorter span of time. The playbook for these earlier investors is pretty much the same with a few variations.

VIVE was started by an industry veteran, Vartan Jerian, Jr., who sold his independent MSO to Caliber and then honed his executive talents within that organization. After exiting Caliber, he joined up with two private equity sponsors and two alumni of other private equity firms who had spent years looking at the industry.

CollisionRight was sponsored by Center Oak Partners, a relatively small private equity firm with deep experience in the automotive aftermarket. They backed an experienced leader, Rich Harrison, who had executed a platform and roll-up strategy at TruRoad Holdings. In just four years, Collision Right grew to more than $300 million in revenues, beginning with a modest sized platform in Ohio and Kentucky.

New Mountain Capital backed a deeply experienced management team of former ABRA executives, led by Toan Nguyen, the former Chief Information Officer and Chief Strategy Officer at ABRA. His team acquired Atlanta-based Classic Collision as its initial platform and proceeded to grow to $1 billion+ in revenue within just four years.

Successor investors have less risky appetites – and must invest larger amounts

As early investors succeed in launching platforms and roll-up strategies with attractive exit multiples, their acquirers are buying with expectations that the risks have been reduced. The predictability of cash flows has increased. The management teams are more proven. The costs of acquisitions and greenfields are more stable and the entire direction of consolidation is more clear. And the very large private equity firms are able to write much larger checks – in fact, they need to write larger checks given the size of their funds.

More private equity investors waiting in the wings

Focus Advisors tracks more than 120 private equity firms that have examined the collision repair industry. Our team has had direct conversations with more than 100 of them over the past 12 months. Some are already well-informed; others are rapidly coming down the learning curve.

Why are so many private equity firms looking to enter the industry? Successful growth and exits by other PE firms are driving much of the interest among new investors. At the recent MSO Summit sponsored by Focus Advisors, a large PE firm in attendance queried us, “Is it too late to initiate an entry?”

For many of these prospective investors, the nuances of the industry often surprise them. There are substantially different challenges in collision repair from the more conventional platform/add-on strategies that have worked so well in other industries. In many of these successful roll-up strategies, individual consumers make purchase decisions. But in the collision repair industry, third-party intermediaries – insurance companies – heavily impact the flows of business through Direct Repair Programs. In addition, the technical skill sets required to create superior gross profits and EBITDA reside in a technical workforce that has been in short supply for a generation.

With more than 80 MSOs with five or more shops that Focus Advisors has identified in its proprietary database, there is no shortage of candidate platform targets, depending upon the appetite of PE investors. While there are relatively few $30 million revenue platforms, there are many in the $15 million+ range. The true scarcity is management teams that are capable of rapid unit growth and attracting the skilled technicians required to staff their platforms.

Conclusions

-

More private equity firms will make initial investments.

Focus Advisors expects the industry will see many new private equity firms entering the market in the next five years. Some will invest to build and flip. Others will buy and build for the longer term. -

Independent MSOs will find attractive partners.

Independent MSOs with strong management teams will continue to find willing capital partners at attractive values. Targets with a stable and growing base of technicians will attract more attention and higher values.

-

Exit opportunities with larger sponsors will increase.

Well-developed private equity-sponsored platforms will continue to find large acquirers, either through consolidators growing by merger or very large private equity firms seeking to buy out early private equity investors.

About the Author

David Roberts

Managing Director, FOCUS Investment Banking LLC

David Roberts is the founder and managing director of M&A advisor Focus Advisors. He is best known for co-founding Caliber Collision Centers with his partner Matthew Ohrnstein in 1997, envisioning a more collaborative repair process across insurance companies, insureds, and repairers. After raising the first private equity capital in the industry, David and his partner began buying, rationalizing, and systematizing collision repair shops into the nation’s first consolidated, performance-based MSO. By the time of its sale in 2008, Caliber was the world’s largest collision repair consolidator, a position it continues to hold today with more than $8 billion in sales.

After leading dozens of acquisitions for Caliber, David saw an opportunity to help other MSO owners achieve superior results in growing and selling their businesses. He founded Focus Advisors Automotive M&A with a proven method to help them grow, thrive, and prepare for a strategic exit. Over the past ten years, David has led $500 million in 35 separate automotive transactions. Today, Focus Advisors, a FINRA-registered investment bank, has grown to include a team of eight professionals, all committed to the same mission of helping MSO owners realize the full value of what they’ve worked so hard to build.

Focus Advisors has invested in creating a comprehensive and proprietary database of the entire collision repair industry including the largest consolidators, private equity investors, more than 800 MSOs and 25,000 single shops, including dealers. The firm also tracks transaction values from large MSOs to single shops and everything in between which allows them to provide the best informed valuation advice to its many clients.

David received his B.A. from Duke University and his MBA and J.D. from University of California, Berkeley. He is married to Gail Simpson. Together, they have two daughters and a new grandson!