Focus Advisors Releases 2025 Mid-Year Review of MSO Activity

Editor's note: Focus Advisors released its “2025 Mid-Year Review: Consolidation Continues Despite Headwinds.” It is printed here in its entirety.

The first half of 2025 (“H1 2025”) brought a complex mix of pressures for collision repair operators nationwide. Elevated total loss rates continue to shrink the pool of repairable vehicles, with nearly one in four appraisals now resulting in a total loss — a trend driven by rising repair costs, aging fleets, and declining used-vehicle values. According to CCC, the average Total Cost of Repair (TCOR) rose just 1.1% year-over-year through Q1 — the slowest pace of increase since 2009 — but still high enough to keep insurers and consumers cost-conscious. For both single-shop independents and large MSOs, these factors — combined with persistent margin pressure from insurers and ongoing staffing challenges — have made the first half of 2025 a period of renewed focus on efficiency and disciplined operations.

Yet despite the challenging environment, consolidation continued with several interesting developments:

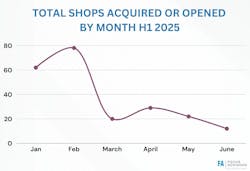

1) Total deals are down. Focus Advisors’ proprietary data shows deal volume slowed during H1 2025. The total number of shops acquired or opened by Consolidators and market-leading MSOs for the first six months of this year was 223, down 35% compared to the same period in 2024 (343).

However, a closer look at the charts shows the decline is concentrated among three of the Big Five — Caliber, Crash Champions, and Joe Hudson’s — who pulled back. Gerber was flat year over year, while Classic Collision increased openings.

That slowdown reflects a variety of factors: cash-flow constraints, softer earnings, seller pushback on valuation expectations, and possibly the overhang of Caliber’s anticipated IPO. Meanwhile, mid-sized regional buyers acquired or opened 4.5% more stores in H1 2025 vs. H1 2024, even as the Big Five’s combined openings plus acquisitions fell 60.3% year over year.

2) Caliber’s potential IPO. On July 28, Caliber Holdings, Inc., the parent of Caliber Collision Centers, confidentially submitted a draft registration statement (Form S-1) to the U.S. Securities and Exchange Commission for a proposed initial public offering. A confidential filing allows a company to talk privately with institutional investors, receive feedback from the SEC without public scrutiny, and retain strategic flexibility concerning timing and execution of the actual IPO.

3) Private equity continues its aggressive move into collision repair. Private equity interest in the industry is easy to understand: car accidents, hail damage, and other collision repair needs are non-discretionary, and insurers typically foot the bill. The industry is sufficiently large, suitably fragmented, and sustainably profitable. The Romans Group estimates the total addressable market for the US collision repair industry is $48 billion per year. Many also believe the industry is recession-resistant, and AI will not be replacing body techs anytime soon. Even if claim counts dip from economic shifts or ADAS technology, rising revenue per repair — driven by more complex vehicles and continued increases in parts and labor costs — keeps collision repair an appealing, resilient investment for private equity.

PE firms have closely followed the successful recapitalizations of VIVE, Collision Right, Classic, and Crash Champions over the last few years. Last year, Focus Advisors spoke with more PE firms about collision repair than ever before, and we now track a list of more than 130 firms that have expressed interest in entering the industry. This year, that interest is turning into action: three new entrants on the East Coast, one in the Midwest, and one on the West Coast. Over the past three years, PE firms have also shifted their initial investment strategies, showing a greater willingness to enter the space through smaller acquisitions with modest growth goals before scaling up. For example, three of the new entrants began with acquisitions of just three or fewer shops.

4) Chilton and OpenRoad appoint a new CEO. We just learned that Chilton Auto Body, a 20-location platform in Northern California owned by PE firm Trive Capital, has hired former Fix Auto USA, OEC, and Gerber executive Paul Gange to lead their enterprise. In April, OpenRoad Collision named Steve Horton as its new Chief Executive Officer. Horton brings deep experience from Caliber Collision, where he held senior leadership roles and drove geographic expansion. At OpenRoad, he will lead the company’s next growth phase, focusing on disciplined expansion and operational execution. OpenRoad currently has 28 collision repair locations across Texas, Arizona, Oklahoma, and New Mexico.

5) VIVE and Brightpoint accelerate expansion. VIVE Collision added three centers in January alone, bringing its footprint to 63 locations across 10 Northeastern states. VIVE Collision entered its 10th state, Delaware, in August 2025 with the acquisition of Evolve in New Castle. Throughout H1, however, they acquired shops in Pennsylvania (Professionals Auto Body), Massachusetts (Lund Collision and Carsmetics of Worcester), New York (Sprague’s Collision Center), Vermont (Clark’s Collision and Rotunda’s Collision Center), New Jersey (Lamon Auto Body, Lee’s Auto Body, and Executive Collision), and Maine (Maine Collision Center).

Brightpoint Auto Body Repair accelerated its pace of acquisitions so far this year. The platform, sponsored by SouthWorth Capital Management, was formed in October 2022 with the acquisition of an MSO in Louisiana. It started the year 2025 with 13 locations and by the end of H1, had grown to 34 locations with acquisitions in Michigan, Ohio, Pennsylvania, Maryland, Georgia, and Tennessee. In the third quarter we expect they’ll complete the acquisition of a client of ours, a three-shop MSO in the Midwest.

6) Total losses continue to rise. According to CCC Intelligent Solutions, in Q1 2025, nearly 24% of all claims were total losses, up sharply from prior years. For non-comprehensive losses involving vehicles seven years or older, total loss rates jumped from 64.7% in 2020 to 74.4% in Q1 2025. Aging fleets, rising repair costs — especially for electric vehicles and ADAS-equipped vehicles — and declining used-car values are collectively eroding repairable volume, tightening margins, and dampening growth for both independents and MSOs.

7) The Big Five keep getting bigger. Even with fewer acquisitions, the increase in brownfield and greenfield openings continues to drive total shop counts for the largest consolidators. According to our research, the Big Five now operate at least 4,019 locations. Collectively, they hold 13.3% of shop market share and approximately 31.7% of revenue market share nationwide. At the end of 2024, only 6 months earlier, that revenue share was just 30%, underscoring that — even with limited shop-count growth in H1 2025 — the Big Five continue to extract value from prior acquisitions and refine their models to provide national solutions for national insurers.

While the Big Five largely stayed quiet during the first half of 2025, history suggests this won’t last. In fact, Gerber recently acquired a eight-location MSO in Northern Virginia and reiterated its goal of adding 400 more sites in the coming years through both acquisitions and new developments.

8) Tesla continues to open corporate-owned shops. Tesla’s strategy to aggressively expand its own national body shop network appears to be creating additional competition for Tesla work in some larger markets. Reports of this have surfaced on both coasts, and have caused some owners to rethink whether they want to continue to invest in the certification. As of this writing, Tesla operates 56 corporately owned locations across the U.S., up five from the beginning of the year, with most of the new additions of Tesla-owned and operated stores in California.

As 2025 progresses, collision repair operators will continue to contend with rising total losses, cost pressures, and cautious insurer behavior. Yet consolidation shows no signs of slowing. Private equity, midsize regional MSOs, and eventually the Big Five are all expected to increase activity. The industry’s fundamentals — non-discretionary demand, increasing repair complexity, and resilient margins — continue to make it an attractive space for investment, even amid challenging conditions.